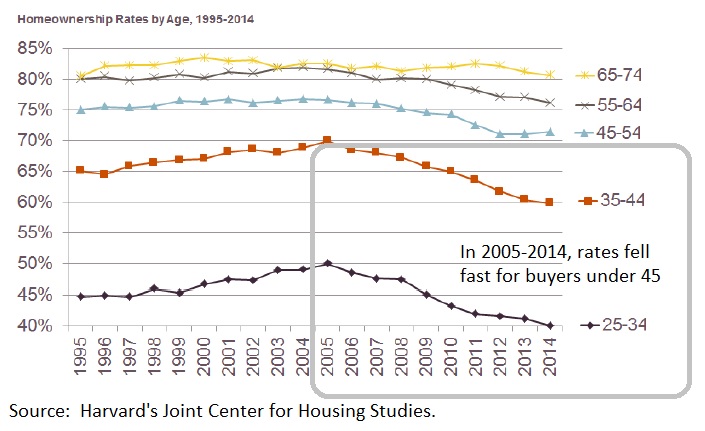

Economic pressures and demographic shifts are preventing many young Vermonters and their peers nationwide from becoming home owners. To help Vermont continue to reap the well-documented benefits that homeownership brings to individual households, their neighborhoods and the greater community, policy makers can create tools that make home buying more economically feasible. Efforts to reduce the upfront financial burden of down payment and closing costs could help retain young Vermonters who might otherwise choose to buy homes in a state with lower home prices and put homeownership within reach of would-be first time homebuyers who will otherwise continue renting.

Economic pressures and demographic shifts are preventing many young Vermonters and their peers nationwide from becoming home owners. To help Vermont continue to reap the well-documented benefits that homeownership brings to individual households, their neighborhoods and the greater community, policy makers can create tools that make home buying more economically feasible. Efforts to reduce the upfront financial burden of down payment and closing costs could help retain young Vermonters who might otherwise choose to buy homes in a state with lower home prices and put homeownership within reach of would-be first time homebuyers who will otherwise continue renting.

Vermonters pay higher closing costs than the national average. The average Vermont homebuyer making a five percent down payment would need to save a whopping $19,000 for closing costs, down payment and secondary market loan fees—as much as a minimum wage worker earns in a year. Buyers who are able to obtain a mortgage requiring only a three percent down payment would still need to bring about $16,000 to the closing table.