Vermont has received over 71,000 unemployment claims since the coronavirus pandemic reached the state. An economic recession is almost certainly forthcoming. This economic disruption will impact Vermont’s housing markets and households, but the full effects will depend on the duration of the coronavirus outbreak.

Unemployment

Vermont’s total labor force as of February was about 340,000 workers. Assuming that all recorded claims are valid, around 21% of Vermont’s workforce has been impacted by the pandemic. This is unprecedented, given that the highest annual unemployment rate experienced in Vermont in the past 44 years was nearly 9% in 1976. However, this data is difficult to compare to past economic crises, given that new categories of workers are eligible for unemployment benefits for the first time, such as self-employed workers or people who are temporarily left without childcare.

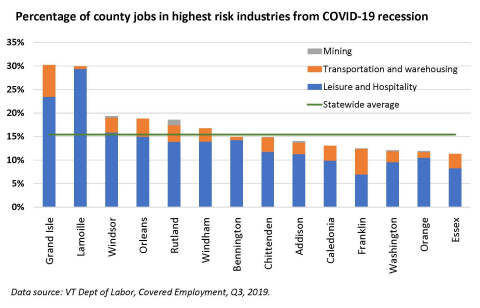

According to Moody’s, the industries likely to suffer most in the new recession are leisure and hospitality, employment services, transportation, mining and travel arrangements. In Vermont, 12% of jobs are in the leisure and hospitality sector and another 3% are in transportation and mining. This is comparable to the 16.5% average among all U.S. metro areas. The number of Vermont jobs in the employment services and travel arrangements industries is not available but likely to be low. In past recessions, Vermont has seen lower unemployment than many parts of the county. Vermont had an unemployment rate of 6.6% in 2009, the height of the Great Recession, compared to 9.9% nationally.

Some Vermont counties may be hit harder than others. In Grand Isle, Lamoille, Orleans, Rutland, Windham and Windsor, more than 15% of the jobs are in the leisure and hospitality, transportation and mining industries. Grand Isle and Lamoille counties have nearly 30% of jobs in these higher risk sectors. Rutland County also is highly vulnerable to the current economic crisis, with 19% of its jobs in higher risk sectors. It has 4,900 jobs in these sectors—more than any county outside of Chittenden County.

Risks due to severe housing cost burden

An increase in unemployment will strain many already struggling Vermont renters and homeowners. An estimated 17,905 renter and 21,245 owners households – accounting for 16% of all Vermont households – are severely cost-burdened, paying more than half of their income towards housing expenses including rent, mortgages and utilities. This put these households at high risk for eviction or foreclosure, even before this crisis.

The rate of cost-burden increased during the last recession and will likely increase again during this period. Although legislation is being enacted to deliver unemployment payments and stimulus checks to households, payments may be slower to reach independent contractors and self-employed workers. Undocumented persons, people who work ‘under the table’ and do not report income, and other people who do not file tax returns are typically ineligible for unemployment and may be ineligible or encounter challenges qualifying to receive stimulus checks. The majority of households with non-traditional employment are lower income, putting them at higher risk for housing insecurity.

There are already signs that many households are unable to make rent payments as a result of the crisis. According to the National Multifamily Housing Council, an estimated 69% of households nationally had paid their April 1st rent on time, compared to 81% in March.

Evictions and foreclosures

Foreclosures on mortgages held through Fannie Mae, Freddie Mac, the Federal Home Loan Banks and USDA Rural Development will not proceed during the crisis, and homeowners through these programs may be eligible for delayed payments and other temporary assistance. While these institutions are responsible for the majority of mortgages in Vermont, any other foreclosures are unlikely to proceed due to the temporary cancelation of most court hearings.

New evictions hearings in Vermont are also temporarily halted, and the Vermont Legislature is currently considering a formal moratorium on evictions. However, there is currently no federal plan for relief for renter households once court proceedings resume and many renters may continue to struggle with rent payments.

Vermont’s housing market during recessions

Despite these concerning indicators, there is reason to believe that the impact of the virus on Vermont’s overall housing market could be relatively brief. During the last recession, Vermont median home prices decreased by just 5% before regaining their full value within five years, although some Vermont towns did experience larger drops in prices. Vermont was better off than the nation as a whole, where the median home price dropped by 19% between 2007 and 2009. The last recession originated within the housing market, exposing a pattern of risky mortgages made on over-valued properties. Although the coronavirus outbreak will cause significant economic distress, it is not specifically impacting the housing or mortgage markets in the same way the last recession did.

At the same time, the overall volume of Vermont home sales declined significantly during the last recession, and have yet to reach pre-recession numbers. Home sales may be slow to resume after the outbreak passes due to the current difficulty conducting showings and appraisals, and many prospective buyers may be less likely to purchase a home during this period of job losses and economic uncertainty. However, in 2019 Vermont saw signs of significant demand from homebuyers, with the highest number of homes sold since 2006. Any potential decrease in home construction will likely not heavily impact Vermont’s home sale numbers, as new home sales represent an extremely small percentage of Vermont’s total sales. Whether Vermont will return to its recent pattern of strong sales or will revert to its recession pattern of low volume likely depends on the duration of economic slow-down.

Strong demand and high prices will likely persist in Vermont’s rental housing market. Vermont’s average rental vacancy rate is an estimated 3.4%, with Chittenden County at an estimated 1.9%. Housing experts consider rental markets to be healthiest with a vacancy rate between 4 and 6%. Even if Vermont rental vacancy rates were to increase somewhat due to more people living with family or friends and more young people waiting to start their own households, the decrease may not be enough to impact rent levels. Vermont median rents did not decrease during the last recession.

Graph data source: VT Dept. of Labor, Covered Employment, Q3 2019. Includes Leisure & hospitality, mining, and transportation/warehouse.